Summary

- Last quarter validated the company's digital strategy when online demand grew by 70% and new online customers more than doubled for both American Eagle and Aerie brands.

- Given that last quarter's gross margins were a royal 5%, it is easy to guess that the only way from here is up.

- The company is exiting the pandemic-driven lockdown with $900 million in liquidity and more than $400 million of net cash on the balance sheet while the broader retail sector is struggling.

We recently bought shares of American Eagle Outfitters Inc. (NYSE:AEO). The company has survived the storm better than peers, as evident from the 95% sales productivity achieved by the company's reopened stores in May, and there are several catalysts for top line growth and margin expansion, including much talked about Aerie, in a market environment where peers will struggle to reestablish the lost ground.

"All birds find shelter during rain but eagle avoids rain by flying above the clouds. Problems are common, but attitude makes the difference"

APJ Abdul Kalam

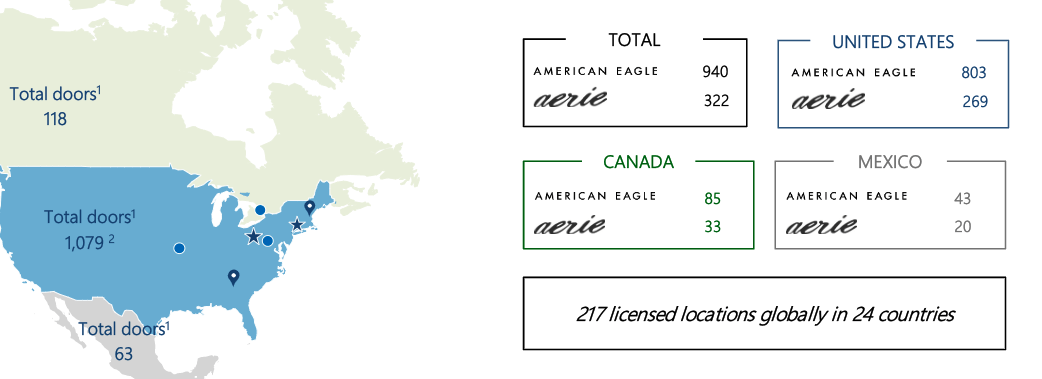

Having been bullish on selective retailers, including Duluth Holdings (NASDAQ:DLTH) that was covered in a note yesterday, we believe the market is waking up to the Aerie brand, which will cross $1 billion in sales this year, and will be forced to recognize several other levers available to American Eagle to reset revenue growth and margin expectations.

Aerie is grossly underappreciated and undervalued

Aerie, the lifestyle brand offering intimates, apparel, activewear, and swimwear for women, is growing fast in a sector that has a major player - Victoria's Secret (NYSE:LB) which is losing rapidly relevance among young women ages 15-25, a perfect opportunity to gain share and lead the space for Aerie. The sell-side is just warming up to the potential, as evident from favorable reports over the last few days.