Summary

- I think shares of Kraft Heinz are trading at ridiculously low valuations at the moment, and I think investors would be wise to buy.

- I think the case of Kraft Heinz demonstrates fairly conclusively that the same company can be either a terrible investment or a great investment.

- In my previous article on the name, I recommended a short put option that worked out very well. I'm doing the same again.

In the few years I've been writing on this forum, I've come out with two articles on Kraft Heinz Co. (KHC). The first of these was bearish and the shares are down about 58%, against a gain of about 5% for the S&P 500. One of my reasons for avoiding the stock back in early January 2018 was the fact that it was trading at a price to free cash of 34 times. Twenty months later, I changed my tune and became quite bullish. The shares subsequently rallied about 10.6% against a loss of about .5% on the S&P 500. I noted that the valuation had moved from the mid-30s to about 12 times cash flow. I write that not to brag (though I'll admit that revealing myself to be a bit of a braggart is a pleasant side effect). I point out my record on Kraft Heinz to once again try to drive home the point I've been droning on about incessantly (and no doubt tiresomely) for years. Namely, the same company can be either a great investment or a terrible investment depending upon the price paid. Kraft Heinz is a great investment when the market gets too pessimistic and drives the shares to ridiculously low levels. Kraft Heinz is also a terrible investment when the market gets too excited about the company's prospects, and seems mesmerized by images of oceans of ketchup splashing all over the world's barbeques and sporting events.

In this piece, I want to try to understand whether the shares currently represent good value or not. I'll make that determination by looking at the sustainability of the dividend, and by looking at the financial history more generally. In addition, I'll look at the stock as a thing distinct from the actual business. In my latest article, I recommended a short put trade, so I'll offer an update on that and will recommend yet another option trade. For those who missed the title of this article, I'll come to the point. I think Kraft Heinz is a great buy at current prices, and I'll go through my reasoning below.

Financial Snapshot

The financial history here indicates to me that Kraft Heinz is somewhat of a cash cow. Both revenue and net income have been in long-term decline. In particular, over the past four years, sales have declined at a CAGR of about 1.2% and net income has been absolutely devastated. The worst time for shareholders was 2018 when the company suffered a near $16 billion goodwill and intangible loss. This has resulted in a slashing of the dividend here, from $2.35 in 2016 to $1.60 over the past four quarters.

Comparing the first quarter of 2020 suggests that the company remains challenged as far as turning revenue into profits goes. In spite of a 3.3% uptick in sales against the previous period, and a 64% decline in goodwill and intangible losses, net income was down about 5.7% relative to the prior period.

Dividend Sustainability

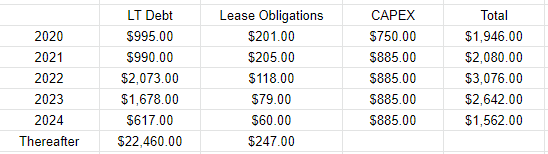

I think investors are interested in whether dividends are sustainable at the current time, given our current circumstances. In order to try to work out how sustainable (or not) the dividend of a particular company is, I am going to compare the upcoming obligations with current assets. I've compiled a list of the upcoming obligations in the table below for your enjoyment and edification. Note that I'm only clear on the CAPEX budget for 2020, as that estimate is found on pp. 33 of the latest 10-K. I've estimated future CAPEX requirements by averaging the previous four years, so CAPEX should be thought of here as a rough estimate.

Source: Latest 10-K

Against these upcoming obligations, the company has an enormous cash hoard of about $5.4 billion. In addition, the company has an undrawn $1 billion credit facility due July 2023. These resources would obviously allow the company to meet its obligations for the next two years at least. For that reason, I consider the dividend to be relatively safe in this case, especially since annual dividend payments have been dropped to below $2 billion.