Summary

- Aqua America is a typical well-run utility, which unsurprisingly makes it a Dividend Aristocrat.

- Despite the risks associated with an entry into the gas utility industry, I believe the company will navigate these challenges reasonably well.

- Aqua America is about as defensive of an investment as one could find, but it's also 17% overvalued.

- Between the 2.2% yield, likely 6-7% earnings growth, and 1.5% valuation multiple contraction, Aqua America is likely to deliver 6.7-7.7% annual total returns over the next decade.

- While I absolutely one day want to own this company, I am looking for an entry point around the company's long-term fair value yield of 2.5%.

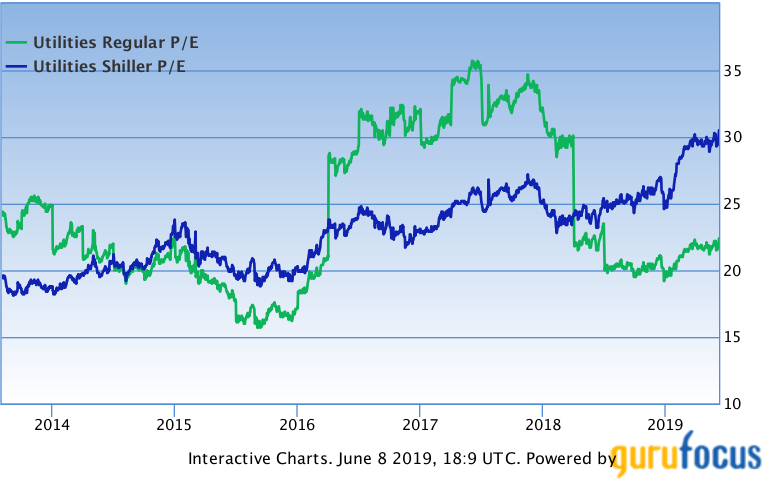

Image Source: Gurufocus

Image Source: Gurufocus

As a dividend growth investor, I am always watching for high-quality companies in defensive sectors trading at fair value or at a discount to fair value.